China local PP and PE market: Post holiday trend in gauge

China local PP and PE market: Post holiday trend in gauge

Chinese players have started the weeklong National Day Holiday and market would only resume trading by 8 October 2018. Regional market participants started gauging the possible market trend in the coming week with hope that demand would remain healthy.

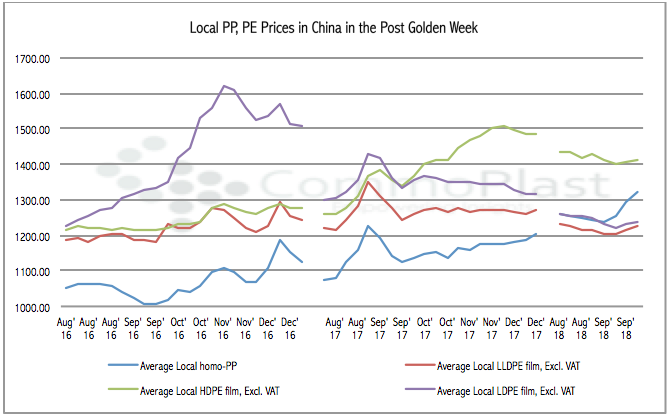

Looking at the historical data, domestic PP and PE market in China tend to remain largely stable to firmer in the post-holiday term in the year 2016 and 2017. The homo-pp market was more constant in maintaining the uptrend over the past two years. Would this trend repeat in 2018?

Looking at the robust purchasing appetite for homo-PP cargoes two weeks before the holiday, it is likely that market would hold strong in the coming weeks, sources said. “A number of traders in China have oversold homo-PP quantity, which means supply might not be too heavy in the post-holiday. In addition to the tight availability and strong upstream costs, we do expect the homo-PP market to repeat the previous years’ trend,” a regional source said.

On the other hand, players are not very confident about the outlook for the PE sector citing the more comfortable supply condition for these grades. “Especially for LDPE film. We have to see the demand from the agriculture sector, which has been delayed this year. Supply for LDPE film is rather ample in the market,” another source added.

Outlook for HDPE and LLDPE film remains cloudy. The fear is that escalated trade war between China and the USA might limit demand for flexible packaging products, though there is still hope for the Single Day Sales. Buyers tend to take a very cautious stance when it comes to making large purchases citing that there is no fundamental support for the large price gap between HDPE and LLDPE.

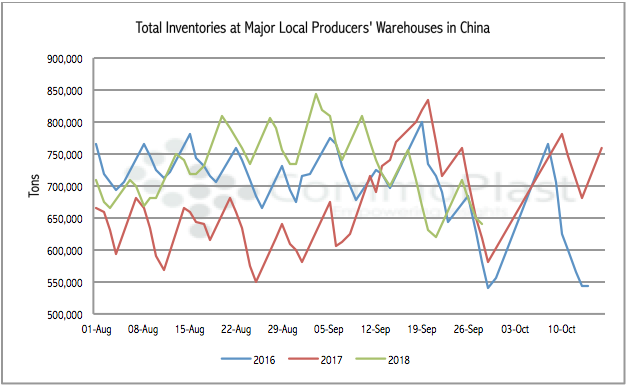

From the supply point of view, total PP and PE inventories at Sinopec and CNPC’s warehouses did not fall sharply during the pre-holiday period as it did in 2016 and 2017. Data showed that by 28 September 2018, total inventories stood at 640,000 tons, while in 2016, this figure has fallen to 555,000 tons and in 2017 to 580,000 tons.

Inventories normally surge about 200,000 tons throughout the holiday week; however, major shutdown at Shanghai Secco and Fujian Refinery & Petrochemical this month might tighten supply a little.