Asian ethylene market slump on weak demand and heavy influx on deep-seas supply

Asian ethylene market slump on weak demand and heavy influx on deep-seas supply

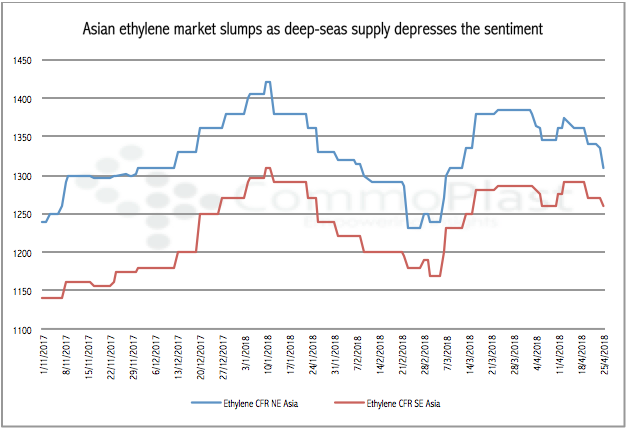

After a brief rebound in mid-April, the Asian ethylene market extended the softening trend this week as buying interest remains weak while supply keeps improving with the available deep-seas cargoes.

Compared to late March, when the market hit the multi-month high levels, ethylene costs based on CFR Northeast Asia has fallen $75/ton to $1310/ton as of 25 April 2018. The CFR Southeast Asia value only shreds $25/ton in the same period to $1260/ton.

The heavy maintenance shutdown schedule at major Asian crackers has not been able to support the market due to the constant influx of cargoes from the USA and Europe. The softening trend might persist in the near term, sources said, especially with the current sluggish downstream PE market.

Import PE market in China receives very limited number of new offers this week due to the on-going ChinaPlas Exhibition, however, by the week ending 20 April 2018, the average import HDPE film to China were reported at $1385/ton, LLDPE film at $1217/ton and LDPE film at $1220/ton, all based on CFR China, LC 0 -90 days term. All of these cargoes are priced below the theoretical costs based on the current ethylene costs.

In the meantime, ethylene cost in the USA has fallen to the lowest level since 2002, leaving the arbitrage window wide-open. More ethylene supply in the USA would emerge as several new crackers come online this year while downstream PE plants in the country are slow to ramp up causing supply to outpace demand.

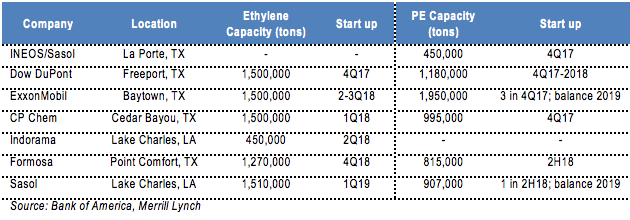

Followings are the start up schedules at new crackers and PE plants in the USA from 2017 to 2018.