Local China PP, PE market might extent journey north as inventories pressure reduce

Local China PP, PE market might extent journey north as inventories pressure reduce

Domestic market in China has been recovering from the Lunar New Year blue since late March, though prices are not firming up too significantly given the fact that suppliers’ main focus is on depleting the bloated stock levels.

Compared to the final week of March 2018, when offers for both PP and PE hit the cyclical bottom, the market has firmed up approximate $15-20/ton on an average for both grades. This trend is expected to persist in the near term, especially with the manufacturing season soon to start.

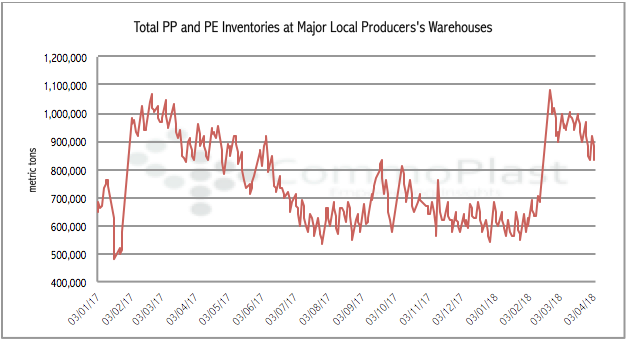

Private data combined by CommoPlast showed that the apparent inventory pressure on major local producers, including Sinopec and CNPC, has reduced evidently since early March 2018. Just before the market went off for the Tomb-sweeping holiday, total PP and PE inventories on major producers’ hands fell to approximate 830,000 tons. This is a result of an extensive effort in stimulating local demand while switching production to non-commodity grade for better margins. In fact, local homo-PP injection grade has been commanding a premium of CNY100-150/ton ($16-24/ton) for two weeks straight, which is relatively attractive to producers.

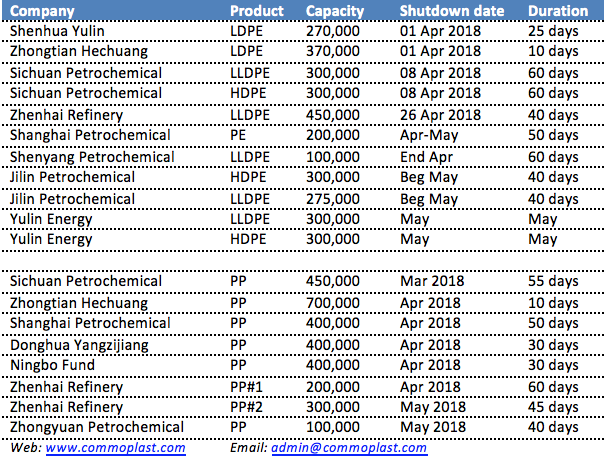

Besides the better purchasing interest for local materials, the market is expecting supply to tighten in the coming month amid heavy maintenance shutdown in April and May.

Though players are generally expecting a firmer trend in local PP and PE market in the near term, yet, it appears that most local suppliers are still putting heavy attention on depleting inventories, which might limit the extent of any possible price surge. “Until domestic inventories reduce to below the 700,000 tons mark, we are not expecting any major hike in local offers,” a market source added.