What is going on in China PP market?

What is going on in China PP market?

As CommoPlast reported earlier, the post Lunar New Year demand condition in China is far below market expectation resulted in the accumulation of inventories. In addition to the high number of import cargoes arrival, especially for USA origin, China market is bloated for more than a month now.

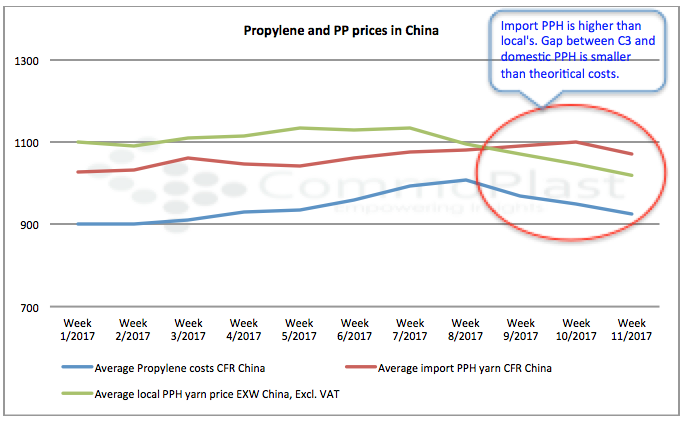

Domestic ground therefore constantly going down since mid February, encouraging a number of traders to divert their cargoes to other markets for better profit margins. In contrast, international suppliers are in no rush to reduce their offers claiming limited supply stemming from a number of shutdown and healthy demand in Western market. This has led to an unusual condition where import homo-PP are traded at premium compared to domestic cargoes.

Weak demand in the PP market has also pulled the upstream propylene (C3) lower in spite of a series of cracker shutdown. Even with that, the gap between propylene based on CFR China and local PPH based on EXW China term is still about $50/ton below the theoretical costs of about $150/ton. In another word, it is uneconomical for Chinese producer to produce PP at the current spot propylene prices. Therefore, players are expecting a correction to bring market back to the normal condition.

A market source commented, “It is hard for domestic prices to surge drastically amid the current inventory level. It would make more sense that international suppliers step back on their offers, given falling upstream costs and also weakening Southeast Asian demand.”

A Middle Eastern producer added, “We are still monitoring further development since buying interest in local China market is on recovery track. In addition, we are not having high inventories on hand. There might be a small adjustment given the sluggish condition across Asia, yet, we are not expecting any significant adjustment.”