Asian ethylene market tumbled on weak demand

Asian ethylene market tumbled on weak demand

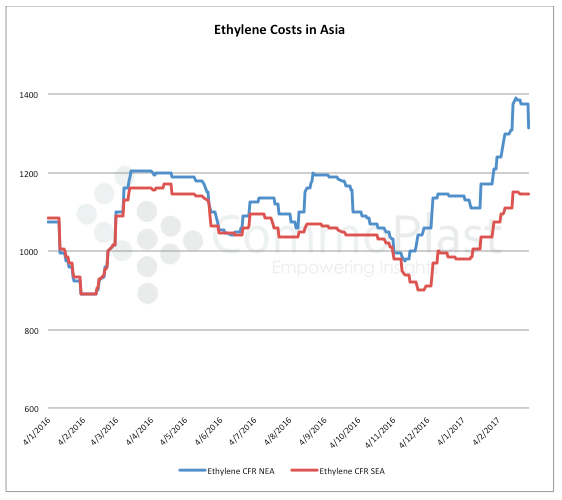

After reaching the multi years high level during late February 2017 due to robust demand from the styrene monomer sector, ethylene cost based on CFR Northeast Asia has been steadily softening, shredding $60/ton in a single trading day last Friday. In contrary, ethylene cost based on CFR Southeast Asia term holds steady over the past nearly two weeks.

Players believed that this is a technical correction as ethylene prices, especially in the Northeast Asia region was artificially pushed up with only support from styrene monomer sector, while the largest ethylene derivative segment – polyethylene (PE) remains weak.

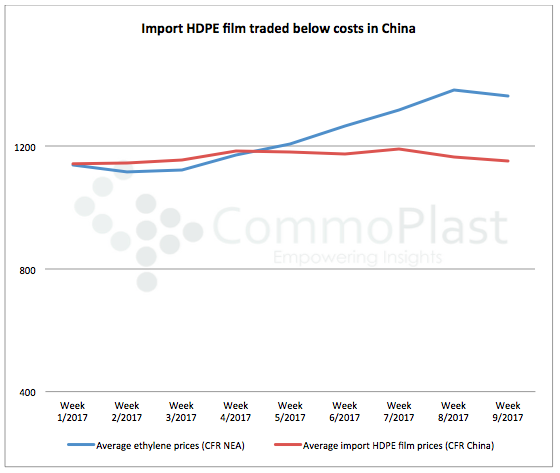

In fact, according to CommoPlast data, import HDPE film based on CFR China term spend much of the first nine weeks of the year traded below the ethylene costs, with the largest gap recorded during late February at minus $220/ton instead of the theoretical breakeven point at positive $150/ton.

The question most popularly asked at the moment is that would ethylene prices continue to move lower in the coming day despite a series of regional and overseas crackers are undergoing maintenance shutdown, which could tighten the supply. The answer market participant mostly sided is – yes. For the fact that not only PE derivative is suffering from serious negative margins, but also the styrene monomer market is falling, narrowing the profit margin.

A market source added, “There must be a correction as most downstream market is unable to support the current prices. We expect ethylene costs in both Northeast Asia and Southeast Asia region to narrow the location gap to a reasonable range. We expect market continue to witness adjustment this week before it could be stabilized by the second half of the month.”