Ethylene cost continue to hold premium over PE in China

Ethylene cost continue to hold premium over PE in China

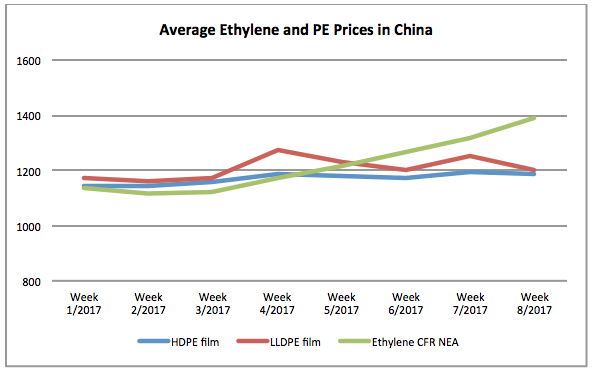

As reported earlier, a series of major regional crackers undergo maintenance shutdown has tightened the availability of spot ethylene in Asia. In addition, to strong demand from the styrene monomer (SM) sector, ethylene costs in Northeast Asia region has steadily firming up since the third week of the year, to reach the highest level since November 2014.

Such drastic increment in ethylene costs have supported sentiment in the downstream PE market, keeping prices on the stable trend despite sluggish post holiday demand condition in China. However, PE prices are now trailing behind its own production costs by the gap of nearly $100/ton as shown in the following graph.

Healthy ethylene demand has prompted many major regional crackers to increase operation rate. According to the Japan Petrochemical Industry Association, steam cracker run rate in the country averaged at 100.1% in January, up from 98.4% in December and the output also rose 2% from a month earlier to 590,100 tons. In addition, many international PE producers are seeking better margins in the upstream ethylene market, from which several have decided to cut operating rate at the downstream plants.

A market source commented, “This is not very sustainable as PE remain the largest ethylene derivative and demand has been really sluggish over the past month. Inventories in China are pilling higher than usual. We prefer to take cautious stance in the coming weeks as it seems market might be nearing the peak.”