|

|

Limited supply pushes Asian ethylene market higher despite weak downstream marketLimited supply pushes Asian ethylene market higher despite weak downstream market |

|

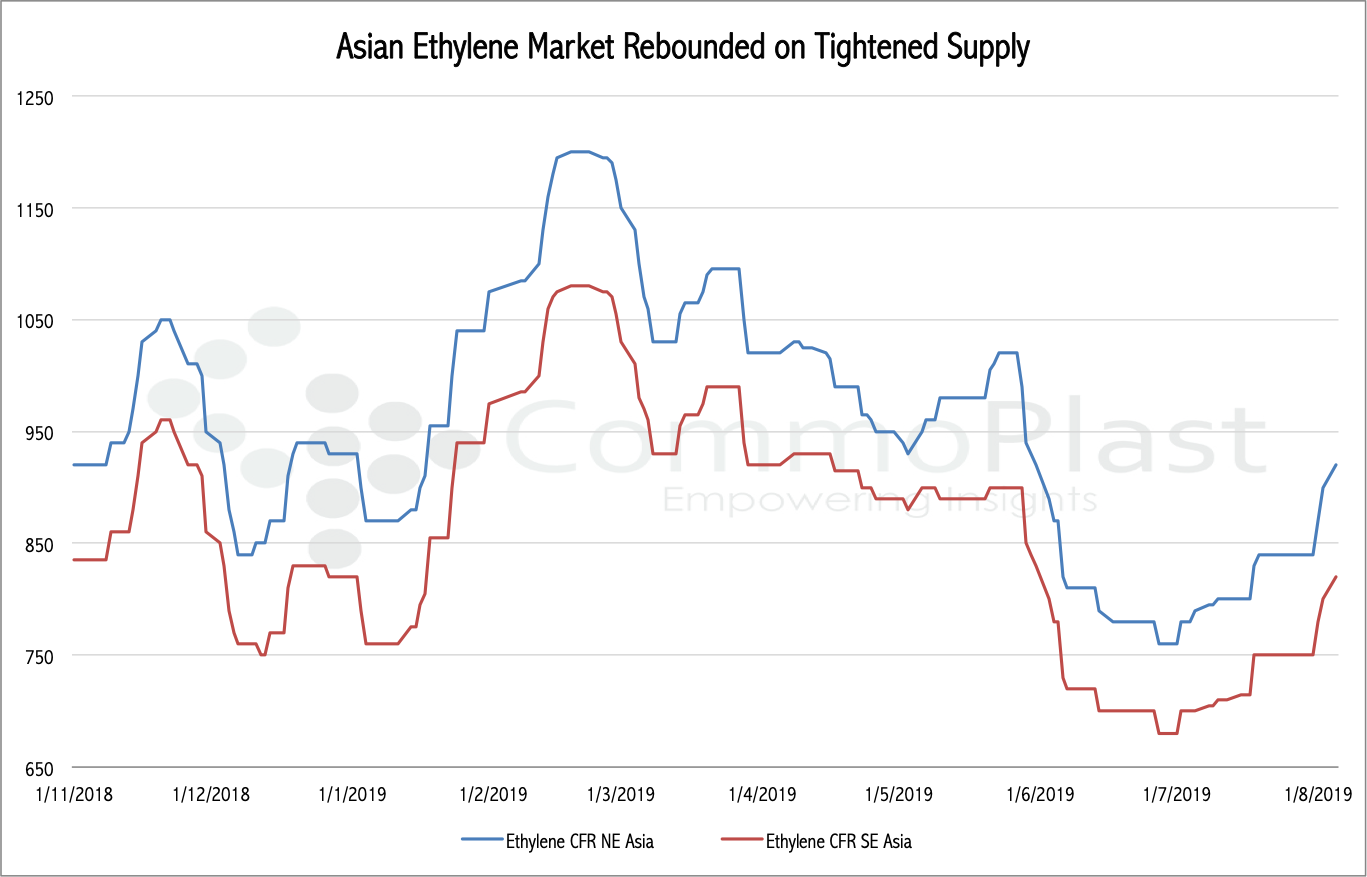

The Asian ethylene market tightens slightly in recent weeks, which supports a strong rebound since the beginning of July 2019. Data from CommoPlast suggests that import ethylene costs based on CFR Northeast Asia jumped $160/ton from the cyclical bottom at the beginning of July to $920/ton as of 5 August 2018.

Hanwha Total has not been able to operate its naphtha cracker in Daesan smoothly since the beginning of the year. After a labour strike that delayed the restart following the debottlenecking work in March, the cracker was again shut during late July due to a lightning strike. The 1.41 million tons per year cracker has resumed operation on 28 July, sources said, however, remain operating at a low rate.

Besides, the recent fire at ExxonMobil plant in Baytown, USA has stimulated the sentiment to a certain extent. One of the cracker with a capacity of 1.8 million tons/year has been shut due to the incident, however, the company refused to reveal further detail on the damage condition.

A number of market participants commented that the shutdown at Formosa and Petronas might curtail the availability to Northeast Asia and support the firming trend in the near term. In the meantime, it is important to note that demand from the downstream PE market might drop as trading activities in this sector become more sluggish following the escalated trade war between China and the USA, of which currencies are weaponized.

On 6 August 2019, the average import HDPE and LLDPE film to China based on CFR China term fell approximately $5-10/ton from last week.

Country

China