|

|

Asian ethylene hits six months high on supply concern; sustainability uncertainAsian ethylene hits six months high on supply concern; sustainability uncertain |

|

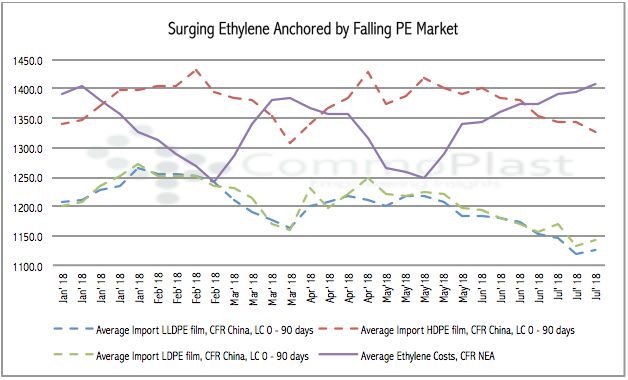

The Asian ethylene market, specifically the Northeast Asia region, has hit the highest level in six months as tightened supply and healthy demand in Japan cushion the increases. At the time this report is published, CFR Northeast Asia value stands at $1410/ton, however, the probability of further hike also reduced significantly.

Looking at the supply side, sources reported production issues at major Japanese operators that bite into spot availability. Due to unspecified mechanical glitches, both Keiyo Ethylene and Maruzen Petrochemical were forced to slash operating rate to 70% late last week and might remain in this condition for the next two to three months. Meanwhile, Mitsui Chemical delayed the restart to mid-August after a fire hit the petrochemical complex on 21 June 2018. The market is expected to lose nearly 180,000 tons of ethylene production from these production hiccups.

On a contrary, industry participants are raising concern that the current trend might prove short-lived given the lack of support from the largest ethylene derivative sector – polyethylene (PE).

Import PE to China has been constantly moving lower since mid-May and see sharper reductions in the recent days thanks to the weakened purchasing interest, stemming from fear of escalated trade war, depreciated local currencies that make imports more expensive and the traditional off-peak season.

CommoPlast data suggests that the average import HDPE film to China is now about $80/ton below ethylene cost while the average LLDPE film and LDPE film prices are about $260-270/ton into the negative zone. “Chinese customers are resisting the current ethylene levels, which might curl the uptrend,” an industry source commented.